Conventional wisdom dictates that your portfolio should be diversified, but as this article suggests, a ‘Diversified Fund’ may not be the best way for you to achieve diversification.

What is a Diversified Fund?

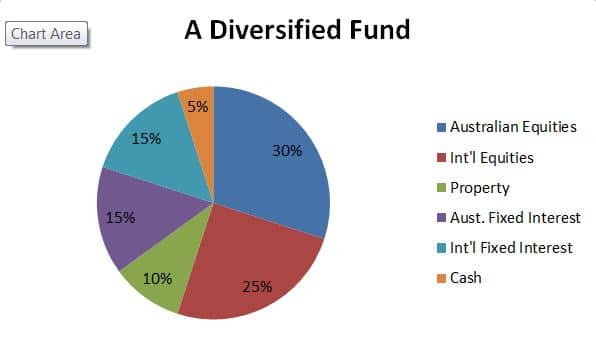

A diversified fund is simply a managed fund which invests into a number of different asset classes as opposed to just one asset class. These asset classes are generally Shares (International & Australian), Property, Fixed Interest (International & Australian) and Cash.

Product providers will typically offer a number of different diversified funds such as “Balanced Fund”, “Growth Fund” etc. The Growth Fund may have an 80% weighting to the growth assets (Shares & Property) whereas the Balanced Fund may have a 65% weighting to growth assets. A Balanced Fund is the most common as it is usually the “default” investment for your superannuation; it’s invested automatically into the Balanced Fund until you decide to change investment options.

In the past most financial planners and investment advisers recommended Diversified Funds for their clients, however the trend is now towards constructing a portfolio of specialist, asset class specific, managed funds (and/or direct shares). The end result is that the client still has a diversified portfolio, but has more choice, and more control, over their investment.

I believe there are a number of shortfalls in having your super invested in a Diversified Fund. These include:

1. Retirement Planning

The GFC was an ugly time for investors. As we now know, and as history has consistently shown, selling growth assets during severe bear markets results in wealth destruction. The ideal situation would be to ride it out, however if you were in retirement mode and drawing a pension, you legally had to make withdrawals. People invested in Diversified Funds were therefore selling a portion of all asset classes with each withdrawal – with each $100 withdrawn, x% came from Australian Shares, x% from International Shares and so on.

A portfolio constructed of sector specific funds will allow the investor to withdraw from just the cash portion and let the growth assets remain. Sure, the growth assets will drop just like the growth portion in the diversified fund, but at least you have the option of not selling them, and therefore a greater ability to recover from the falls.

2. Funds chosen may not be the best

The Diversified Fund will typically allocate each asset class portion to a different sector specific fund. There is a temptation for XYZ Balanced Fund to allocate the Australian component to XYZ Australian Share Fund, the International component to XYZ International Share Fund, and so on. Now XYZ may happen to be an excellent fund manager for Australian shares, but it is highly unlikely (almost impossible) for them to excel as a fund manager for all asset classes.

A portfolio constructed of sector specific funds will allow the investor to invest in top rated fund managers for each of the asset classes, regardless of which company the top rated fund manager is from.

3. Control and Investment Options

Fund Managers normally have set benchmarks they must adhere to. For example, Australian Equities may have a benchmark of 34% with a minimum exposure of 31% and maximum of 37%. A Diversified Fund is therefore not the investment of choice for someone who would like a more active approach towards asset allocation. Neither is it the choice for an investor who would like to geographically target their International exposure to say Asia, Europe or Emerging Markets.

If your super is sitting in a diversified fund somewhere, please arrange an appointment so you can investigate alternative options.